Learn the key differences between emergency funds and savings accounts. Discover how much to save, where to keep it, and real-life examples. Complete guide for Indians.

If you’re serious about building financial security, understanding the difference between an emergency fund and a savings account isn’t just helpful—it’s essential. While both involve setting money aside, they serve completely different purposes in your financial life. Getting this distinction right can mean the difference between weathering life’s storms with confidence or spiraling into debt when unexpected expenses strike.

According to recent surveys, a staggering 75% of Indians don’t have an emergency fund and could default on their EMIs in case of sudden job loss or income disruption. This alarming statistic reveals a critical gap in financial planning that leaves millions vulnerable to financial shocks. Let’s explore how you can avoid being part of this statistic by mastering both emergency funds and savings accounts.

What is an Emergency Fund?

An emergency fund is a dedicated pool of money set aside exclusively for unexpected, urgent expenses that you cannot plan for. Think of it as your financial safety net—a buffer that protects you when life throws curveballs your way.

Common emergencies that require this fund include:

-

Medical emergencies not fully covered by insurance

-

Sudden job loss or income reduction

-

Urgent car repairs after an accident

-

Critical home repairs like a burst pipe or damaged roof

-

Family emergencies requiring immediate financial support

The primary purpose of an emergency fund is to prevent you from relying on high-interest credit cards, personal loans, or disrupting your long-term investments when crisis strikes. Research from Vanguard shows that having at least ₹1.5 lakh ($2,000) in emergency savings significantly reduces financial stress and improves overall well-being.

How Much Should You Save in Your Emergency Fund?

Financial experts universally recommend maintaining 3 to 6 months’ worth of essential living expenses in your emergency fund. However, the exact amount depends on your personal circumstances:

-

Single individuals with stable jobs: 3 months of expenses

-

Married couples with dependents: 6 months of expenses

-

Self-employed or business owners: 9-12 months of expenses

-

Single-income families: 10-12 months of expenses

Example Calculation:

If your monthly essential expenses are ₹50,000 (covering rent, groceries, utilities, EMIs, school fees, and insurance), your target emergency fund would be:

-

Basic level: ₹1.5 lakhs (3 months)

-

Recommended level: ₹3 lakhs (6 months)

-

Higher security: ₹5-6 lakhs (10-12 months for single-income families)

Don’t feel overwhelmed by these numbers. Even starting with ₹10,000 to ₹20,000 provides immediate peace of mind and protection against minor emergencies.

What is a Savings Account?

A savings account is a more flexible financial tool designed to store money for planned goals and future purchases. Unlike an emergency fund, this money is earmarked for things you anticipate and actively work towards.

Common uses for savings accounts include:

-

Vacations and travel plans

-

Festival shopping and celebrations

-

Buying new gadgets or electronics

-

Home improvement projects

-

Wedding expenses

-

Down payment for a vehicle or property

The amount you maintain in your savings account is entirely goal-based. If you’re planning a ₹1.5 lakh vacation, that becomes your savings target. For a ₹5 lakh car purchase, you set your monthly contributions accordingly.

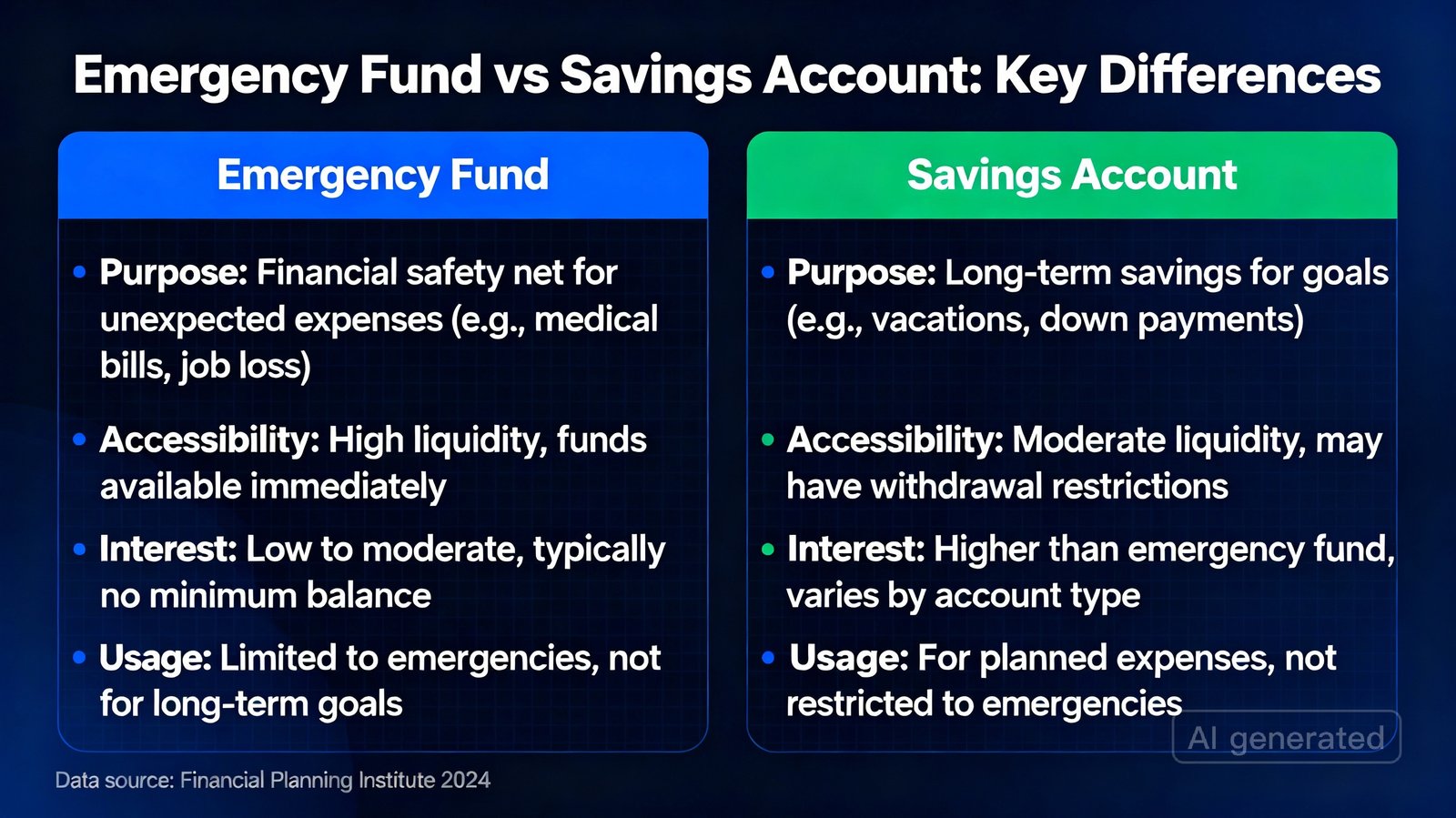

The Critical Differences: Side-by-Side Comparison

Understanding the distinctions between these two financial tools helps you allocate your money wisely and maintain both security and progress toward your dreams.

| Feature | Emergency Fund | Savings Account |

|---|---|---|

| Primary Purpose | Cover unexpected, urgent expenses (medical bills, job loss, car repairs) | Save for planned goals and future purchases (vacation, gadgets, down payment) |

| Usage | Only for genuine emergencies | For achieving specific financial goals |

| Recommended Amount | 3-6 months of essential living expenses (₹1.5-6 lakhs for most Indians) | Goal-based – varies by objective (₹50,000 for vacation, ₹5 lakhs for car) |

| Access Speed | Immediate to 1-2 days | Instant access anytime |

| Best Account Type | High-yield savings account, Liquid funds, Money market funds | Regular savings, High-yield savings, Recurring deposits |

| Risk Level | Very low – capital protection is key | Very low – stable and secure |

| Flexibility | Low – should not be touched except for emergencies | High – can withdraw anytime for planned expenses |

| When to Use | Medical emergencies, sudden job loss, urgent home/car repairs, income disruption | Vacations, festivals, buying electronics, home improvement, wedding expenses |

Real-Life Case Study: How Rajiv and Meena Built Their Emergency Fund

Let’s look at an inspiring real-life example from Jaipur that demonstrates the power of systematic emergency fund building.

The Situation:

Rajiv and Meena, a working couple in Jaipur with two school-going children, had zero savings when the COVID-19 pandemic hit in 2020. They faced simultaneous salary cuts and a health emergency that left them financially vulnerable and stressed. After the crisis stabilized, they committed to never being caught unprepared again.

Their Plan:

-

Monthly household expenses: ₹45,000

-

Emergency fund goal: ₹2.7 lakhs (6 months of expenses)

-

Strategy: ₹5,000 monthly SIP in a Liquid Fund

-

Timeline: 9 months to reach their target

The Execution:

Rajiv and Meena automated their savings by setting up a Systematic Investment Plan (SIP) that transferred ₹5,000 monthly from their salary account to a liquid mutual fund. This automation removed the temptation to skip months or spend the money elsewhere. They also:

-

Cut down on dining out and unnecessary subscriptions

-

Redirected festival bonuses to the emergency fund

-

Sold unused items online to generate extra contribution

The Result:

Within 9 months, they successfully built their ₹2.7 lakh emergency fund. The real test came in 2023 when their daughter contracted dengue, requiring hospitalization. The medical expenses not covered by insurance totaled ₹45,000. Thanks to their emergency fund, they paid the bills without stress, borrowing, or disrupting their other financial goals.

The Recovery:

After using a portion of their emergency fund, Rajiv and Meena immediately resumed building it back up. They increased their monthly contribution to ₹7,500 and restored the fund to full capacity within 6 months. Today, they feel proud and secure knowing they can handle life’s surprises without panic.

Another Powerful Example: The Job Loss Scenario

Consider Priya, a 32-year-old marketing professional from Mumbai living in a rented apartment with monthly expenses of ₹60,000. She had diligently saved ₹3.6 lakhs as an emergency fund—exactly 6 months of expenses—stored in a combination of high-yield savings account (₹1 lakh for immediate access) and liquid mutual funds (₹2.6 lakhs).

In March 2024, her company underwent restructuring and she was laid off unexpectedly. While the news was devastating, her emergency fund transformed a potential crisis into a manageable transition period:

-

Month 1-2: Priya focused on job hunting while her emergency fund covered rent, groceries, and EMIs without stress

-

Month 3-4: She used the breathing room to upskill with online courses and attend networking events

-

Month 5: She secured a new position with better pay before depleting her entire fund

Had Priya not maintained an emergency fund, she would have been forced to accept the first available job regardless of fit, borrow from family, or accumulate high-interest credit card debt.

Why You Need Both: The Dual Protection Strategy

Having both an emergency fund and a savings account creates a dual layer of financial protection that serves different but complementary purposes in your financial life.

Without separation, you risk:

-

Derailing your goals: Imagine you’ve saved ₹1.5 lakhs for a long-awaited family vacation. Suddenly, your car breaks down requiring ₹80,000 in repairs. Without an emergency fund, you must raid your vacation savings, postponing or canceling your trip and disappointing your family.

-

Creating a savings shortfall: When you mix funds, it becomes difficult to track progress toward specific goals. You might think you have enough saved, only to realize you’ve inadvertently spent your emergency cushion.

-

Increasing financial stress: Research shows that people with dedicated emergency funds experience 20% less financial stress and spend 3 fewer hours per week worrying about money compared to those without.

-

Falling into debt traps: Without emergency savings, unexpected expenses force you to rely on credit cards (with 20-40% annual interest) or personal loans, creating a debt spiral that’s hard to escape.

The separation allows your savings goals to progress uninterrupted while your emergency fund stands ready to protect your financial foundation.

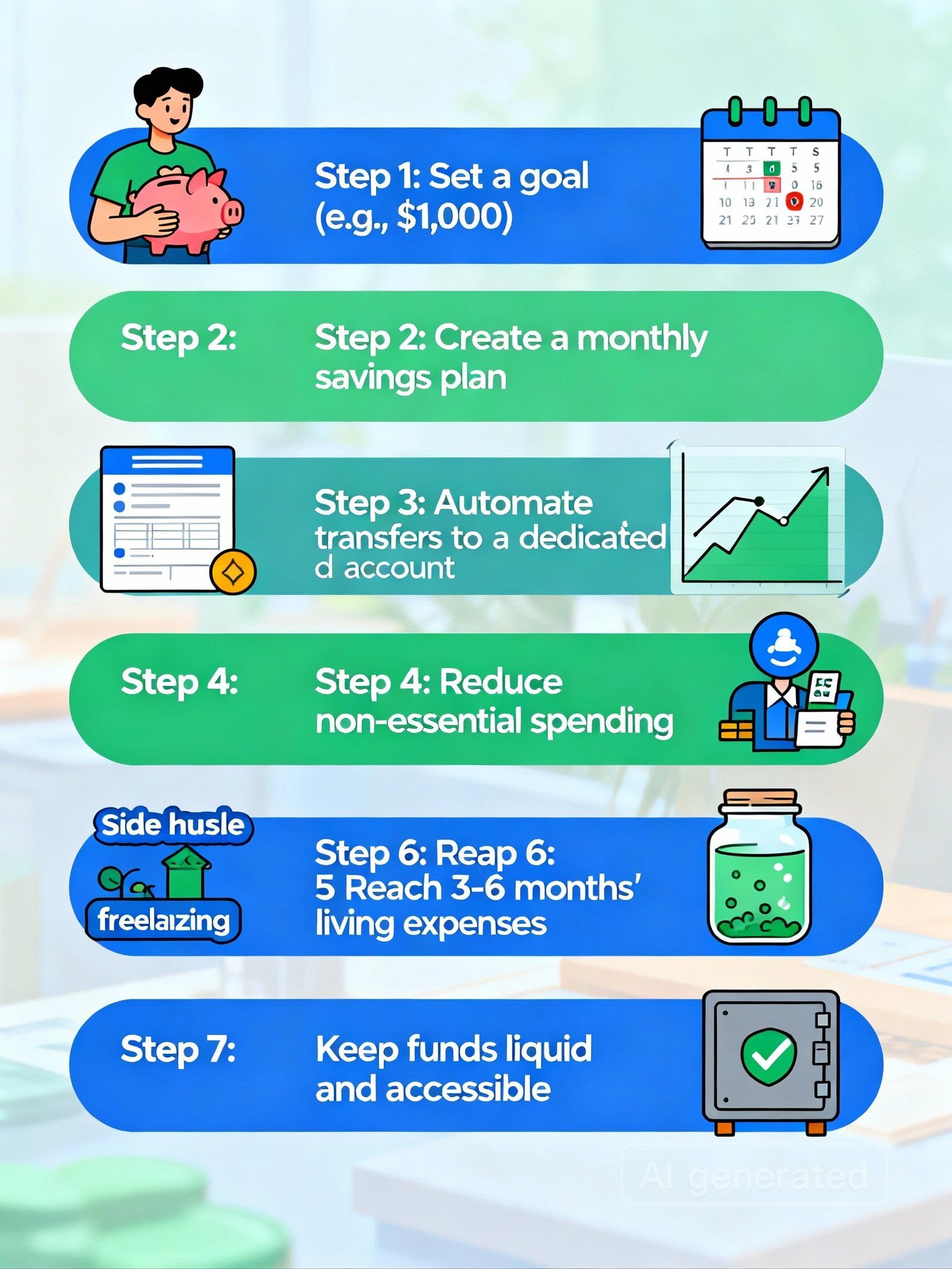

Step-by-Step Guide: Building Your Emergency Fund from Scratch

Even if you’re starting with zero savings, you can build a robust emergency fund by following this proven strategy:

Step 1: Calculate Your Essential Monthly Expenses

Start by identifying your non-negotiable monthly costs—expenses that must be paid regardless of circumstances:

-

House rent or home loan EMI

-

Groceries and essential food

-

Utilities (electricity, water, gas, mobile)

-

School fees and education costs

-

Health-related expenses and medications

-

Insurance premiums

-

Existing EMIs and debt payments

-

Transportation (fuel or public transport)

Exclude: Entertainment, dining out, shopping, hobbies, and luxury expenses. These can be cut during emergencies.

Step 2: Set Your Emergency Fund Goal

Multiply your essential monthly expenses by your target number of months (3, 6, or 12 based on your situation):

Example:

-

Monthly essential expenses: ₹40,000

-

Target: 6 months (recommended for families)

-

Emergency fund goal: ₹2.4 lakhs

Step 3: Start with a Mini-Goal

If ₹2.4 lakhs feels overwhelming, break it into manageable milestones:

-

Mini-goal 1: ₹10,000 (covers small emergencies)

-

Mini-goal 2: ₹50,000 (covers moderate emergencies)

-

Mini-goal 3: ₹1.2 lakhs (3 months of expenses)

-

Final goal: ₹2.4 lakhs (6 months of expenses)

Celebrating each milestone keeps you motivated throughout the journey.

Step 4: Open a Separate Account

Create a dedicated account exclusively for your emergency fund—never mix it with your regular savings or checking account. This physical separation:

-

Reduces temptation to spend on non-emergencies

-

Makes tracking progress easier

-

Creates a psychological barrier against casual withdrawals

Best options for parking your emergency fund:

-

High-yield savings account (3-4% interest) – Instant access

-

Liquid mutual funds (6-7% returns) – Access in 1-2 days

-

Money market funds (6-7% returns) – Access in 1-2 days

Recommended split: Keep 30% in savings account for immediate needs, 30% in short-term FD, and 40% in liquid funds for better returns while maintaining reasonable access.

Step 5: Automate Your Contributions

Set up automatic monthly transfers from your salary account to your emergency fund account. This “pay yourself first” approach ensures consistent savings regardless of temptations:

-

Schedule the transfer for your salary day

-

Start with whatever you can afford—even ₹2,000-₹3,000 monthly makes a difference

-

Increase the amount by 10-20% whenever you get a raise or bonus

Step 6: Find Extra Money to Accelerate Growth

Speed up your emergency fund building by finding additional sources of income or savings:

Income boosters:

-

Freelance work or side hustles

-

Selling unused items online

-

Part-time consulting in your area of expertise

Expense reducers:

-

Cancel unused subscriptions (OTT platforms, gym memberships, magazines)

-

Pack lunch instead of eating out

-

Reduce delivery app usage

-

Negotiate lower rates on insurance or mobile plans

Windfall deposits:

-

Tax refunds

-

Festival bonuses or Diwali bonuses

-

Gifts or inheritance

-

Annual increment or performance bonuses

Step 7: Protect Your Fund with Clear Rules

Establish strict guidelines for when you can access your emergency fund:

✅ Valid emergencies:

-

Medical emergencies not covered by insurance

-

Sudden job loss or significant income reduction

-

Urgent home repairs (burst pipe, broken water heater)

-

Critical car repairs needed for work commute

-

Family emergencies requiring immediate support

❌ NOT emergencies:

-

Vacations or travel

-

Festival shopping or celebrations

-

Buying new gadgets

-

Fashion and lifestyle purchases

-

Planned home improvements

When in doubt, ask yourself: “Is this unexpected, urgent, and necessary?”

Common Mistakes to Avoid

Learning from others’ mistakes helps you build a stronger emergency fund faster. Here are the 7 most common emergency fund mistakes and how to avoid them:

1. Not Starting Early Enough

Many people wait until they have “extra money” before starting an emergency fund. The reality? There’s never a perfect time, and waiting leaves you vulnerable. Solution: Start with just ₹1,000-₹2,000 monthly. Small consistent contributions compound over time.

2. Keeping Your Fund in the Wrong Place

Some people make the mistake of investing emergency funds in:

-

Stocks or equity mutual funds (too volatile for short-term needs)

-

Long-term fixed deposits with penalties for early withdrawal

-

Real estate or physical gold (takes too long to liquidate)

-

Retirement accounts like PPF or EPF (penalties and restrictions)

Solution: Keep your emergency fund in highly liquid, low-risk options like high-yield savings accounts or liquid mutual funds where you can access money within 1-2 days without penalties.

3. Using It for Non-Emergencies

The biggest threat to emergency funds is treating them as a “flexible savings account” for wants rather than genuine needs. Dipping into the fund for a new phone, vacation, or festival shopping defeats its entire purpose.

Solution: Keep your emergency fund in a separate bank or institution from your daily banking to create a physical and psychological barrier.

4. Not Saving Enough

Many people stop after saving ₹50,000-₹1 lakh, thinking it’s “good enough.” But inadequate funds leave you partially protected—you might handle small emergencies but still struggle with major ones like job loss or serious illness.

Solution: Follow the 3-6 month rule based on your personal circumstances, and regularly review your target as your lifestyle and expenses change.

5. Ignoring Inflation and Lifestyle Changes

An emergency fund built 5 years ago with ₹2 lakhs might not be sufficient today if your expenses have increased to account for a bigger apartment, children’s education, or higher cost of living.

Solution: Review and adjust your emergency fund annually, especially after major life changes like marriage, having children, or taking on new financial responsibilities.

6. Forgetting to Rebuild After Use

Using your emergency fund for a genuine emergency is exactly what it’s designed for—but many people forget to replenish it afterward, leaving themselves vulnerable to the next crisis.

Solution: The moment your financial situation stabilizes after an emergency, immediately resume (or even increase) contributions to rebuild your fund.

7. Relying Solely on Credit Instead

Some people skip building an emergency fund entirely, believing credit cards or personal loans can serve the same purpose. This is a dangerous misconception that leads to high-interest debt cycles.

Solution: Build your emergency fund first before focusing aggressively on other financial goals. It’s the foundation of all financial security.

Building Your Savings Account Goals

While your emergency fund protects you from the unexpected, your savings accounts help you achieve your dreams and planned milestones. Here’s how to effectively manage goal-based savings:

Multiple Savings Accounts Strategy

Consider opening separate savings accounts for different goals to maintain clarity and motivation:

-

Vacation Fund: ₹1.5 lakhs for a family trip to Goa

-

Car Purchase Fund: ₹5 lakhs for down payment

-

Wedding Fund: ₹8 lakhs for upcoming wedding expenses

-

Home Improvement Fund: ₹2 lakhs for renovations

This separation prevents you from accidentally spending your vacation money on home improvements or vice versa.

Calculate Your Monthly Contribution

For each savings goal, work backward from your target:

Example: Vacation in 12 months

-

Target amount: ₹1.5 lakhs

-

Timeline: 12 months

-

Monthly savings needed: ₹12,500

If ₹12,500 is too much, either extend your timeline to 18 months (₹8,333/month) or adjust your vacation budget.

Balance Both Priorities

The ideal financial approach maintains both emergency protection and goal achievement. A simple allocation strategy:

For someone earning ₹75,000/month after taxes:

-

₹45,000 for essential expenses

-

₹10,000 for emergency fund (until fully funded)

-

₹10,000 for goal-based savings

-

₹10,000 for investments and long-term wealth building

Once your emergency fund reaches its target, redirect that ₹10,000 to accelerate your savings goals or investments.

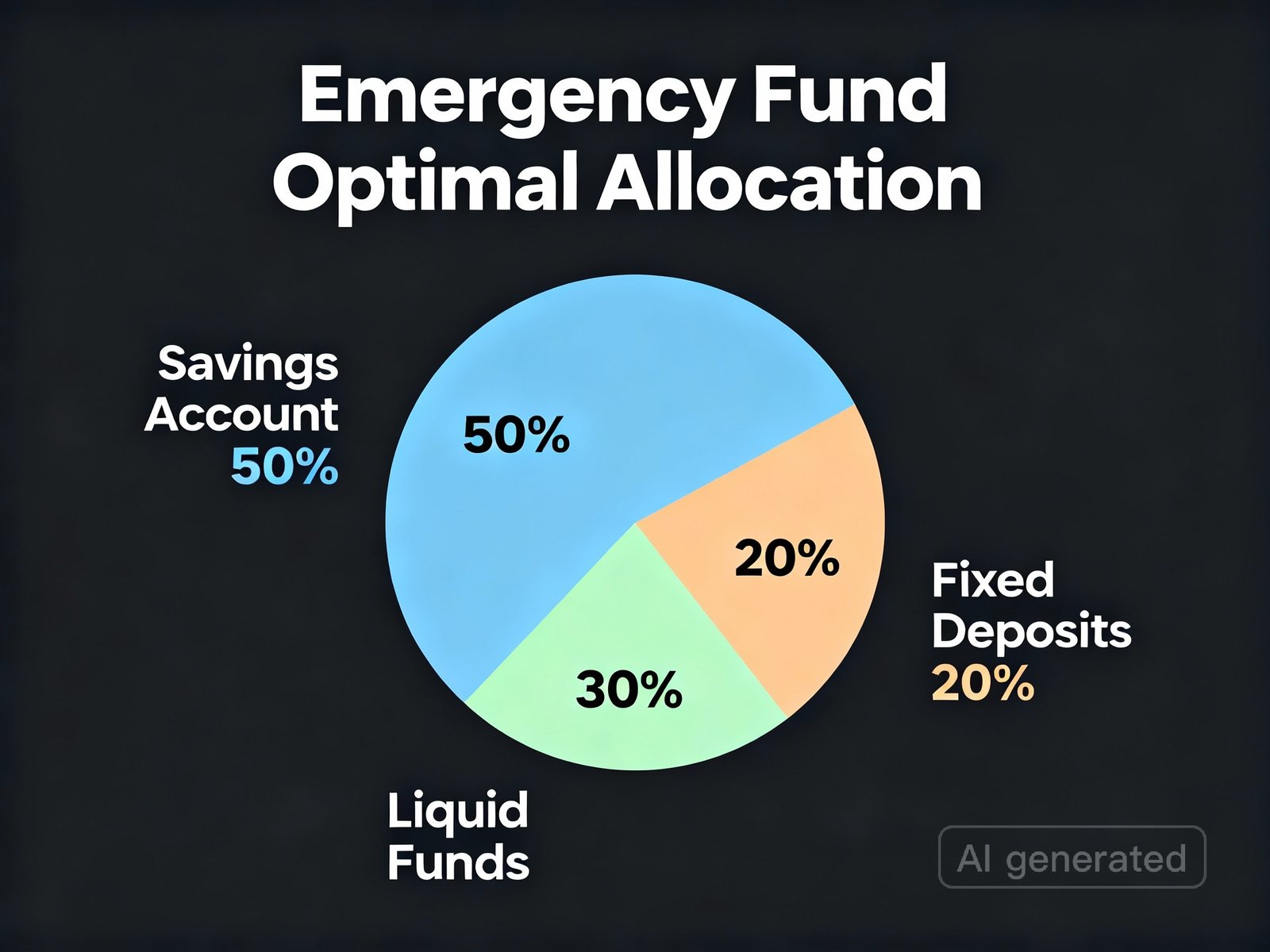

Where to Park Your Emergency Fund: India-Specific Options

Choosing the right parking place for your emergency fund balances three factors: safety, liquidity, and returns. Here are the best options for Indian savers:

Option 1: High-Yield Savings Account (30% of fund)

Returns: 3-4% per annum

Access: Instant (ATM, UPI, net banking)

Safety: Very high – DICGC insured up to ₹5 lakhs

Best for: Immediate emergency needs (1-2 months of expenses)

Option 2: Liquid Mutual Funds (40% of fund)

Returns: 6-7% per annum

Access: 1-2 business days (some offer instant redemption up to ₹50,000)

Safety: High – invests in short-term debt instruments

Best for: Bulk of your emergency fund for better returns

Key advantage: Liquid funds typically offer double the returns of savings accounts while maintaining reasonable access.

Option 3: Short-Term Fixed Deposits (30% of fund)

Returns: 5-7% per annum

Access: Available with premature withdrawal (small penalty)

Safety: Very high – DICGC insured up to ₹5 lakhs

Best for: Portion of fund you’re less likely to need immediately

The Optimal Mix

For a ₹3 lakh emergency fund, consider this allocation:

-

₹90,000 in high-yield savings account (instant access)

-

₹1,20,000 in liquid mutual funds (1-2 day access, better returns)

-

₹90,000 in short-term FD (7-day access, highest returns)

This ladder approach ensures you always have immediate access to some funds while earning better returns on the rest.

SEO Best Practices for Personal Finance Blogs

As you build your Budget Beacon platform, incorporating SEO best practices helps your valuable content reach more readers who need this guidance. Here are key strategies:

Target Keywords for This Topic

Primary keywords to naturally incorporate:

-

Emergency fund vs savings account

-

Difference between emergency fund and savings

-

How to build emergency fund India

-

Emergency fund calculator India

-

Best place to keep emergency fund

-

Savings account vs liquid funds

-

Financial safety net India

-

Emergency fund mistakes to avoid

Action Plan: Get Started Today

Building financial security doesn’t require perfection—it requires action. Here’s your immediate next steps:

Today:

-

Calculate your essential monthly expenses

-

Set your emergency fund goal (multiply by 3, 6, or 12 months)

-

Open a separate account for your emergency fund

This Week:

-

Set up automatic monthly transfer to your emergency fund

-

Review and cut one unnecessary expense

-

Redirect that money to your fund

This Month:

-

Identify your top 3 savings goals

-

Calculate required monthly contributions

-

Create separate accounts or labels for each goal

This Year:

-

Build emergency fund to at least 3 months of expenses

-

Make progress on your primary savings goal

-

Review and adjust quarterly based on life changes

Remember: The best emergency fund is one that actually exists. Starting with ₹5,000 today is infinitely better than planning to save ₹50,000 “someday”.

Final Thoughts: Your Financial Peace of Mind

The difference between an emergency fund and a savings account might seem technical, but mastering this distinction empowers you to take control of your financial life with clarity and confidence.

Your emergency fund is your financial armor—protecting you from life’s unexpected battles. Your savings accounts are your financial wings—helping you soar toward your dreams and aspirations. Together, they create a complete financial system that both protects and propels you forward.

With 75% of Indians lacking proper emergency funds, you have the opportunity to join the prepared 25% who can face financial challenges without fear. Start small, stay consistent, and watch your financial confidence grow with each passing month.

The journey to financial security begins with a single step—and that step starts today. Your future self will thank you for the peace of mind and freedom that comes from being prepared for whatever life brings.

Have questions about building your emergency fund or savings strategy? Drop a comment below! Budget Beacon is here to guide you toward financial clarity and security.